How Long Will $750,000 Last in Retirement?

When you picture your retirement, you may envision relaxing, traveling, or spending more time with family. But behind that vision is an important question: How long will your money last?

Specifically, how long will $750,000 last in retirement? For many retirees, $750,000 is a meaningful nest egg. But whether it will last throughout your retirement depends on several factors that go beyond the balance itself. Let’s explore how you can think about stretching $750,000 over the years and the strategies that can help make it last.

The Role of Withdrawal Strategy: Why the Plan Matters as Much as the Balance

A good starting point when estimating how long your money might last is to use a withdrawal rule of thumb like the 4% rule. This guideline, based on historical market returns, suggests that you can withdraw 4% of your starting balance, adjust those withdrawals for inflation each year, and have a reasonable chance of not running out of money for at least 30 years.

If you apply this to $750,000, that comes out to $30,000 per year in withdrawals.

But while the 4% rule is helpful, it’s also just a rule of thumb - it doesn’t account for personal variations like unexpected healthcare expenses or changes in spending habits. That’s why it’s important to treat it as a starting point, not a guaranteed outcome. Planning is an iterative process. It’s rarely to best to “Set it and forget it”. (Sorry, Ron Popeil)

What Can Shorten - or Lengthen - Your Money’s Lifespan?

Market Returns and Timing

Returns play a role in how long your money lasts, which is why it’s so important to chose an asset allocation that supports your withdrawal plan and retirement needs. Timing also matters. A series of poor returns early in retirement, known as sequence of returns risk, can cause your portfolio to deplete faster than you might expect. On the flip side, strong returns early on can provide more flexibility later. Fortunately, a good plan accounts for this and mitigates and the risk.

Inflation’s Silent Erosion

Even mild inflation quietly eats away at your purchasing power over time. What $30,000 covers today might require $36,000 or more in 10 years. Without accounting for inflation in your withdrawal strategy, your spending power will erode, even if your portfolio balance looks the same.

Lifestyle and Spending Needs

Your personal spending choices also make a big difference. Do you plan to travel extensively in your early retirement years, or do you envision a more modest lifestyle? Small adjustments like cutting back discretionary spending during market downturns can help preserve your savings.

Other Income Streams Can Lighten the Load

For most retirees, Social Security provides a reliable source of income. By coordinating withdrawals from your portfolio with your Social Security benefits, you can reduce the pressure on your $750,000. For example, delaying Social Security until age 70 can increase your monthly benefits and provide a larger cushion later in retirement.

Some retirees also consider part-time work or rental income as ways to supplement withdrawals, helping reduce the withdrawal rate on their savings.

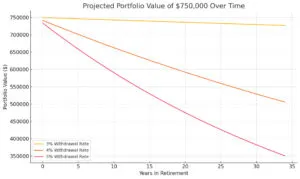

How Long Will $750,000 Last in Retirement: Chart

Here’s a chart showing how $750,000 might last under different withdrawal rates, assuming a 5% average return and 2% inflation.

What the Chart Tells Us

Looking at the chart, you can see how the rate at which you withdraw money from your portfolio has a powerful impact on how long your $750,000 might last.

-

At a 3% withdrawal rate, your money lasts comfortably beyond 30 years. In fact, because your portfolio is earning more than you’re withdrawing (even after accounting for inflation), your balance actually grows over time. This offers a lot of security but might feel overly cautious if it limits your lifestyle early in retirement.

-

At a 4% withdrawal rate, your savings still last right around 30 years, aligning with the classic 4% rule. It strikes a balance between enjoying your retirement and preserving your funds for the long haul.

-

At a 5% withdrawal rate, your portfolio begins to decline much faster. In this scenario, your savings might be depleted in just over 20 years. This higher withdrawal rate can be tempting if you want to spend more early in retirement, but it comes with a greater risk of running out of money later. However, notice that in this scenario about half the money still remains after 30 years.

Key Takeaways: How Long Will $750,000 Last in Retirement?

With a 4% withdrawal rate and withdrawing $30,000 per year you can reasonably expect $750,000 to last and even grow throughout retirement, assuming average market returns and inflation.

-

Reducing your withdrawal rate to 3% can help your savings last longer - likely well beyond 30 years - providing more security.

-

Increasing your withdrawal rate to 5% could mean running out of money sooner, especially if markets underperform.

But life rarely follows neat rules. Markets fluctuate, your spending needs change, and unexpected events happen. Factors like market returns, inflation, lifestyle choices, and Social Security timing can all affect how long your savings last. The most important strategy is to stay flexible, adjust as needed, and coordinate withdrawals with other income sources to make your money go further.

Belonging Wealth Management is a fee-only fiduciary financial planning firm serving Longview, TX and surrounding East Texas towns. We help clients build investment portfolios aligned with their retirement goals, risk tolerance, and income needs. If you want a personalized retirement strategy built around your goals, email us at brandon@belongingwealth.com or call 903-471-0624 and we’d be glad to help you.